Here’s a scenario I commonly see. A startup raises $1M in total seed funding to turn their MVP into a real product and figure out a profitable and scalable customer acquisition model. All goes well over the coming 12 months as they reach $75K in MRR while also growing the team to 10 employees. They find themselves setting plans for a Series A round of funding and predict the process will be similar to their seed round but just with venture funds as the primary target and larger check sizes. After eight weeks and zero success, they approach someone like me for advice and the reaction they get is some flavor of this: “a Series A is not just a larger version of a seed round”. This article dives deeper into what exactly that statement means.

Seed Funding

At the point in your company’s evolution when you raise seed funding, you don’t have much in the way of financial results or operational metrics to get investors excited. Instead, all you have is a collection of hope, vision, promise and potential. Basically, co-founders selling their dream to the earliest of professional investors – angels (I’m skipping past friends & family). Everything else is yet to be proven.

When you’re in this phase, the investors have no choice but to spend most of their evaluation on the team (experience, common sense, chemistry, coachability), the idea (is a real problem being solved?) and the market (is it big enough and dynamic enough). They will also likely gauge the viability of your proposed business model (how you will acquire customers and how you will make money) but they won’t expect a 5 year financial model or a real exit strategy.

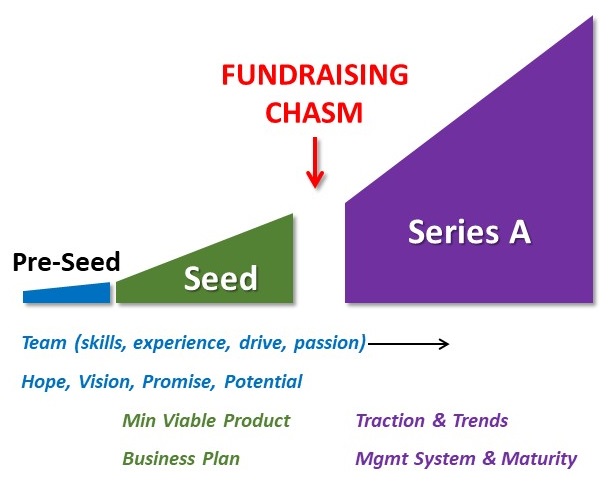

Side Note: Many startups fail to raise enough money in their seed round to directly reach the sweet spot for a Series A. As a result, they call into what I refer to as the “fundraising chasm”. See my article of that same title for more information.

The above graphic highlights the key differences of what investors tend to evaluate during different funding phases. The “fundraising chasm” is shown on the graphic but that’s not the topic of this article.

Series A Funding

By the time you’re ready to raise millions of dollars in a Series A, you have produced a set of measurable results – both financial and operational – and you have evolved into a small but real company versus just a project or experiment. Since the Series A investors have things to poke and prod, that’s exactly what they will do. And since these same investors see tons of deals, they can’t help but “pattern match” you against all others like you. I’m not saying they don’t value your hope, vision, promise and potential. Instead, I’m saying those things must also be supported by recent traction and evolving operational maturity.

Now let’s get more specific about what a typical Series A investor is evaluating:

- Validation

When you started out, you and your co-founders built out a lean business canvas and everything on it represented theories about what could be done. Your mission in life from that stage until you have a sustainable business is to move things from the “theory” list to the “validated” list. Each time you prove something can be done, you either de-risk the investor’s investment or offer them more upside return on investment (ROI) potential. - Traction

The best form of traction for most businesses is paying customers and an accelerating rate of new ones coming on board. In other words, the slope of the results curve matters. And realize that “traction” can also be evidenced in other ways such as signing a truly strategic partnership, garnering coverage from an important industry analyst or convincing an experienced industry veteran to join your advisory board.

* See related article titled “Establishing Valuation Before Revenue Traction” - Customer Acquisition

During your seed phase you acquired customers using whatever methods you had to. But Series A investors will be looking for a repeatable, scalable and profitable method of acquiring customers. To this end, you’ll need to understand your unit economics related to customer acquisition. Those economics are different for each customer acquisition model (ie – self service versus heavy touch).

* See related article titled “Visualizing the Interaction Between CAC, Churn and LTV” - Product

The most important thing the investor is looking for is the level of product-market fit you have demonstrated. In other words, how much have you proven that the world needs your product so badly they are willing to pay for it? They will also evaluate the product’s readiness to scale with the rapid growth that is hopefully about to happen. If it’s not ready for that, you’ll need plans (both technical approach and needed resources). - Team

No doubt, the investors will sense your level of passion and determination. But remember they are investing other peoples’ money and those people don’t care about your or your passion. They just want to get a huge return on their investment due to the huge risk with this class of investment. The investors have no choice but to assess whether you and your co-founders are the ones to get the business venture to the next significant level. If not, it doesn’t mean they won’t invest but it does mean they will need to have a discussion about bringing in some experienced executives. And that could also include a CEO replacement, with the founding CEO either remaining or not remaining in the company. This is when you must ask yourself, “How important is it to be rich versus the king/queen?” - Management System

When the company is made up of 3-4 co-founders, there is no management system. But as employees are hired, results are generated and projects initiated, the company will need a basic management system. You won’t be expected to have a mature culture but you will be expected to describe how you go about making decisions and how you manage the various company activities.

* See related article titled “Establishing a Management System“

I came up with a scorecard approach to determining your Series A readiness. It demonstrates that there is no single scenario for being considered “Series A ready”. You can read it here.

Factors Out of Your Control

The purpose of this article is to differentiate the key investment criteria for an angel-led seed round versus a VC-led Series A. But I would be remiss if I didn’t acknowledge a few other attributes of VC-led investments that could cause your opportunity to either be a fit or not. Do your research ahead of time to make sure you aren’t wasting your time pitching to a VC that isn’t going to invest due to one of the following reasons:

- Stage

I know you’re excited about your $75K in MRR and 10 bad ass employees but some Series A VC’s look for startups that are further down the path than that. - Segment

Most VC’s focus on a short list of either business models, industry verticals and/or technologies. - Target Equity

Many VC’s that lead an investment round require a certain range of equity for their investment (ie – 20-25%). Depending on the amount of money you are raising, their average investment amount and a reasonable valuation, the math might not work out right. - Location

Some VC’s only invest in their local market.

Build Your Roadmap to Series A

Now that you know the sorts of things your future Series A investor will be evaluating, you should paint a picture for what your company should look like for each of those key areas. Then build a roadmap to get you from where you are today to that future state. Regularly check your progress towards the milestones (see related article titled “Try Strategy Horizons Versus a Timeline”) and make sure to adjust your desired future state with any pivot you might make.

Tip: It is a commonly accepted best practice to get to know your potential Series A investors well before you actually are ready to hit them up for an investment (6-9 months is common). If you have a solid roadmap like what’s described above and are able to adopt an “under-promise and over-deliver” approach, tell them what you plan to do over the coming 3, 6, 9 months. Then as you check in with them over time, remind them of this and give them the results. Investors love to see startups that do what they say they’ll do because they realize just how hard that is to accomplish. By the way, that’s the reason to under-promise in the first place.

Here’s a really high-level and simplified way to think about the investor’s mindset at each investment stage:

- (Seed) “Paint me a picture”

- (Series A) “Show me your methods”

- (Series B) “Show me your growth potential”

- (Series C) “Show me your exit potential”

Multiple Seed Rounds Before Series A

Very few startups are able to reach their Series A without multiple rounds of funding during their seed stage. Listen to my 5 minute podcast recording on this exact topic: