Initially made available by Y Combinator (YC) in 2013 and subsequently updated in late 2018, the SAFE investment instrument was intended to improve on the highly popular convertible note used by startups during the seed stage or as a short-term bridge between equity funding rounds. SAFE stands for “simple agreement for future equity” and it is still most popular in California. However, over the years since it’s release it is being used more in other parts of the country.

The purpose of this article is to review the elements that make up a SAFE investment, compare them to a convertible note and generally help both entrepreneurs and investors decide which is  more appropriate for their situation.

more appropriate for their situation.

For those not already highly familiar with how convertible securities work, either read my article titled “Convertible Note Basics” or click the book cover image to read chapter 5 from my bestselling book on fundraising. The free chapter provides a full primer on convertible securities, including a comparison between the SAFE and convertible notes. Click here to order the book.

Or if you’re the audio book type, you can listen to the chapter here:

Before jumping into the review and comparison, I’ll say that until the 2018 SAFE template updates by YC, I wouldn’t have disqualified a personal investment opportunity that uses a SAFE and I wouldn’t push hard on a startup I advise to switch from SAFE to convertible note. However, with the 2018 update, I have a different opinion and it relates to the switch to a post-money treatment of the valuation cap for equity conversion. This change makes the SAFE much less founder friendly because it gives a huge anti-dilution feature to the investors, which means the Common shareholders (ie – founders, employees, advisors) take any extra dilution hit.

As startup attorney Jose Ancer explains in this article titled “Why Startups Shouldn’t Use YC’s Post-Money Safe”, it’s basically similar to the aggressive “full-ratchet” form of anti-dilution protection that Preferred shareholders sometimes try to get, but rarely do

Summary

SAFE is a short, 5-page investment document that is intended to be simple to understand and convenient to administer. It’s not a debt instrument but rather is treated more like a warrant, which is a form of equity. SAFE provides investors the opportunity to convert their investment to equity at a point in the future when a Preferred equity round of funding is raised.

SAFE has many similar features to the well-established convertible notes, such as provisions for early exit (change of control), economic benefits such as the Discount and protection features such as the Valuation Cap. But since the SAFE is not a debt instrument, it doesn’t have a maturity date, which means there is a risk that it never converts to equity and there’s nothing in the terms that call for the investment to be repaid to the investor. There is also now a big difference in the mechanics used to calculate equity upon conversion and I will describe that a little later.

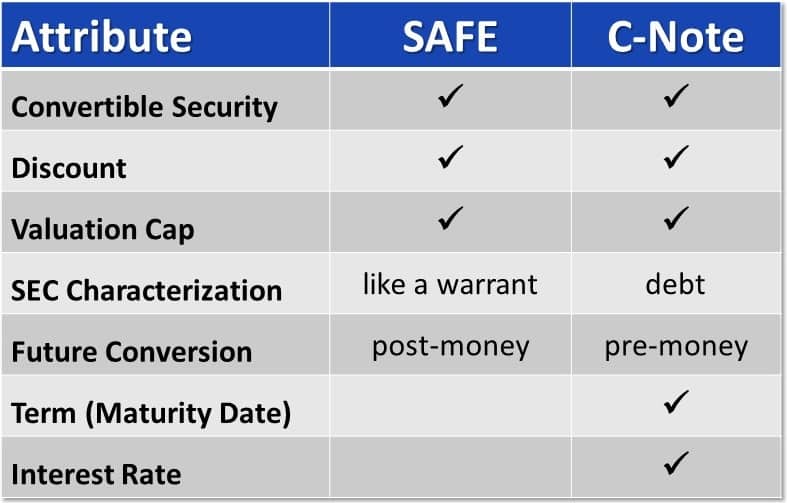

The following table compares the basic features of SAFE to a “typical” convertible note.

Comparing SAFE to a Convertible Note

Now let’s step through the various terms and features one at a time to understand how startups versus investors might evaluate the difference between SAFE and a “typical” convertible note.

Convertible Security

Both instruments are considered convertible securities and the intention of both parties (startup and investor) is for the investment to later convert to a Preferred class of equity

Discount

Both instruments allow for a discount to be applied to the future valuation that is associated with the equity round of funding that causes the SAFE/note to convert. This is one of the key economic benefits to investors.

Note that SAFE templates are available both with and without a discount. I can’t think of a scenario that would justify removing the discount feature but, nonetheless, it’s one of YC’s published options.

Valuation Cap

Both instruments offer the investor the better of the discounted valuation (using the stated discount) or a pre-negotiated valuation cap, whichever is more favorable at the time of conversion. (See my related articles titled “Justifying the Cap Amount in Your Convertible Note” and “Negotiating Valuation“)

Note that SAFE templates are available both with and without a valuation cap. No big surprise here, because there are times when startups remove the valuation cap feature from a convertible note – usually only the most exciting startups that have a lot of interest from investors.

SEC & IRS Characterization

Investors really care what happens to them during a distressed liquidation or dissolution of the company. Since a convertible note is considered a debt instrument, it sits higher in the priority pecking order for getting some of whatever assets are left. The SAFE seems to be positioned ahead of Common equity holders in this regard but not ahead of any secured debt or accounts payable obligations the company has at the time of liquidation/dissolution.

From a tax standpoint, it’s clear that the convertible note is debt. That means if the startup crashes and burns, the investor can write off the full amount as non-business bad debt (I’m not a CPA, which means investors should double-check me on this). The tax loss treatment of a SAFE isn’t as clear. I’ve read that it seems most likely the pre-money version of the SAFE should be treated as a pre-paid forward contract (more on that here) and the post-money version of the safe should be treated as equity (more on that here). From what I’ve read, the convertible note offers much more favorable tax treatment if the company dissolves and the only thing left for the investor is a tax benefit. Investors should double-check all of this with their accountant.

Future Conversion Mechanics

This is by far the biggest change that was made with the 2018 SAFE template update. Before that, SAFE’s converted on a pre-money basis just like typical convertible notes. But the 2018 update calls for SAFEs to convert on a post-money basis. This means that SAFE holders get a more deterministic amount of equity in the future, but they also get some potentially-aggressive anti-dilution rights. That’s because they aren’t diluted by subsequent rounds of funding that utilize convertible securities and also before the next equity funding round that triggers conversion.

The Common shareholders will bear the brunt of all of the extra-described dilution. As startup attorney Jose Ancer explains in this article titled “Why Startups Shouldn’t Use YC’s Post-Money Safe”, it’s basically similar to the aggressive “full-ratchet” form of anti-dilution protection that Preferred shareholders sometimes try to get, but rarely do (as compared to what’s called a “weighted-average” method). Jose later published a proposed fix to the problem and you can read about that in this article.

This single change to the SAFE template swings it from slightly founder-friendly (compared to convertible notes) to very investor-friendly.

Term (Maturity Date)

Convertible notes have them but SAFEs don’t and that’s because a SAFE is not considered a debt instrument.

Investors will not enjoy this aspect of the SAFE because it’s the term (maturity date) feature in convertible notes that forces at least some conversation if there’s no natural conversion to equity over time. Reaching the maturity date on a convertible note also often triggers rights to equity conversion (using a formula that involves the valuation cap). A startup that uses a SAFE and then evolves into a profitable lifestyle business without ever having to sell Preferred equity could leave their investors in limbo forever.

Interest Rate

Convertible notes have them since they are debt instruments but SAFEs don’t.

Seed stage investors don’t make such high-risk investments to accrue 6-8% interest over time but they soon realize that accrual over 18+ months actually adds an interesting amount to the equity conversion formula.

Early Exit Payback

Both offer payout mechanisms to investors if a change of control event (ie – acquisition) happens before a natural conversion to equity.

Note that the SAFE documents are written to give the investor a choice of a 1X payout or conversion to equity using the valuation cap amount to determine equity % and then they can participate in the acquisition along with other equity holders. Most convertible note templates offer an option of a 2X payout or an equity conversion if there’s a change of control. The rationale for the 2X payout is a little more involved that I have space to explain here, but I will say that I agree with it.

Company Type

Often times, startups incorporate as a limited liability company (LLC) rather than as a C-corporation. I won’t entertain that debate in this article, but since a convertible note is a debt instrument, it is usually fine for an LLC to use. However, as written in the template, SAFE appears to require C-corp status since the value of the SAFE investment is reflected on the capitalization table like warrants or stock options. I have heard of LLC’s making some edits to the template so that the SAFE can be used. If this is important to you, check with your accountant and attorney.

Qualifying Transaction

Both instruments call for a conversion to equity when a future Preferred equity round of financing is closed. However, convertible notes stipulate a minimum amount of money to be raised in the future equity round before being considered a “qualifying transaction” that triggers conversion. SAFE investments, on the other hand, convert with any amount raised in a Preferred equity round.

How to Choose?

In California and other mature startup markets, both instruments are probably familiar to most investors. However, if you are trying to raise money in a city where SAFEs are not understood or used often, you don’t want to be the evangelist. Go with the “low friction” approach by using the instrument that’s most commonly used and best understood by seed-stage investors.

From the Startup’s Perspective

- SAFE Advantages: The lack of a Term (maturity date) gives lots of flexibility. The lack of an Interest Rate saves you a little equity dilution in the future when the SAFE converts.

- SAFE Disadvantages: You will bear the brunt of any extra dilution that comes from subsequent rounds of funding using convertible securities before an equity round that converts everything.

- C-Note Advantages: LLC’s can use it without modification.

- C-Note Disadvantages: If you reach the Maturity Date, you’ll either need to request an extension from your investors or somehow close out the Note (payout of principal + interest or convert to equity anyway). The interest that accrues until an equity conversion means slightly more dilution for you and other shareholders.

From the Investor’s Perspective

- SAFE Advantages: Strong anti-dilution protection before conversion to equity. Also the option to convert to equity if the startup gets acquired before a natural conversion (although some C-notes also have this feature). No Qualifying Transaction hurdle to get in the way of an equity conversion.

- SAFE Disadvantages: No Term (maturity date) means no forcing function based on time elapsed. Also no interest accrual to get some time value on the initial investment.

- C-Note Advantages: Has a stated Term (maturity) date that helps force some discussion/action in the future. Offers interest accrual to enhance the potential investment returns. Most offer a 2X return of principal if there’s an early acquisition.

- C-Note Disadvantages: If the Qualifying Transaction term is set too high, the startup could raise a smaller equity round of financing and the Note doesn’t automatically convert to equity.

I guess there’s nothing to prevent a startup from using the 2013 version of the SAFE template and I suspect many will do exactly this. After all, it’s an open-sourced template for a reason. Many startup investors have made tweaks to it over the years.

There are a couple of other miscellaneous points worth mentioning about SAFE:

- Like with any fundraising negotiation, the definition of a “good deal” is represented by a mix of BOTH price (valuation cap) and terms. For more on this, see my related article titled “Tell Me Your Price and I’ll Tell You My Terms“.

- If the startup does well and never needs to raise money via the sale of Preferred shares, they could start issuing dividend payments to Common shareholders and SAFE investors wouldn’t be entitled to participate in those payments.

- Following a conversion to equity, certain rights granted to SAFE investors are based on their original investment amount. This solves what’s sometimes referred to as the “liquidation preference overhang” exposure with most convertible notes. SAFE solves this via a separate series of future preferred stock, commonly called “shadow” or “sub-series” preferred. This certainly seems fair and isn’t something most convertible notes take into account. But it also complicates things with different classes of preferred shares at such an early stage of the company’s lifecycle and seems like it would drive up the legal costs for the future equity round.

The Wilson Sonsini lawyer that created the SAFE instrument, Carolynn Levy, was interviewed roughly a year after the SAFE was introduced to assess the feedback from both startups and investors. You can read the interview here.

Legal Approvals and Filings

Whether you’re incorporated as an LLC or C-corp, you are probably required to document formal approval before raising funding on a convertible note. Check your bylaws (or operating agreement) and confirm with your attorney to make sure everything is done by-the-book. (for more on running a clean company, read my article titled “Accumulated By-the-Book Debt Eventually Comes Due“).

Most funding rounds using convertible notes are not filed with the SEC like equity funding rounds are. But there might be reasons why you should do so, including if you happen to need the Rule 506 Safe Harbor protection the comes with a Regulation D filing. Your attorney is, again, the best one to advise you on this.