I get the following question all the time from US-based startups: how should we price our individual units of equity? (shares of stock for C-corps; units for LLC’s) It’s a very simple question with a not-so-simple answer. The reason is that in the very early days of a startup’s evolution, the methods used to price the company’s stock involve more art than science. Let’s explore further.

Disclaimer: I am not a licensed attorney and I am not a certified valuation professional. The following information results from my own personal experience and conversations with hundreds of startups. You should ALWAYS consult with your attorney and/or accountant for matters as important as setting your stock price. At the end of this article you’ll see additional comments from a certified professional in the field of business valuations.

TL/DR Short Explanation

Some startups will take the company’s valuation they used for a round of funding (or assume they’ll use for an upcoming round) and divide that dollar amount by the total number of shares/units on the cap table to come up with a price per share/unit. The flaw with this logic is the formula they used is more akin to the method used to price a special class of equity that is sold to investors. That equity is often referred to as “preferred” equity due to the special preferential rights that accompany the equity.

Note: For the rest of this article, I will use the word “share” to represent the individual units of equity. But the same concepts generally apply to LLC’s that are incorporated with the concept of equity units.

Before the company raises an equity round of funding, they only have “common” class equity and that equity isn’t near as valuable as the preferred class of equity they will sell to investors. In my experience, and from numerous professional stock valuations I’ve seen performed, common equity ends up discounted in the range of 80% versus preferred equity. In other words, if the preferred stock price is $0.50 per share, the common stock price will be in the range of $0.10.

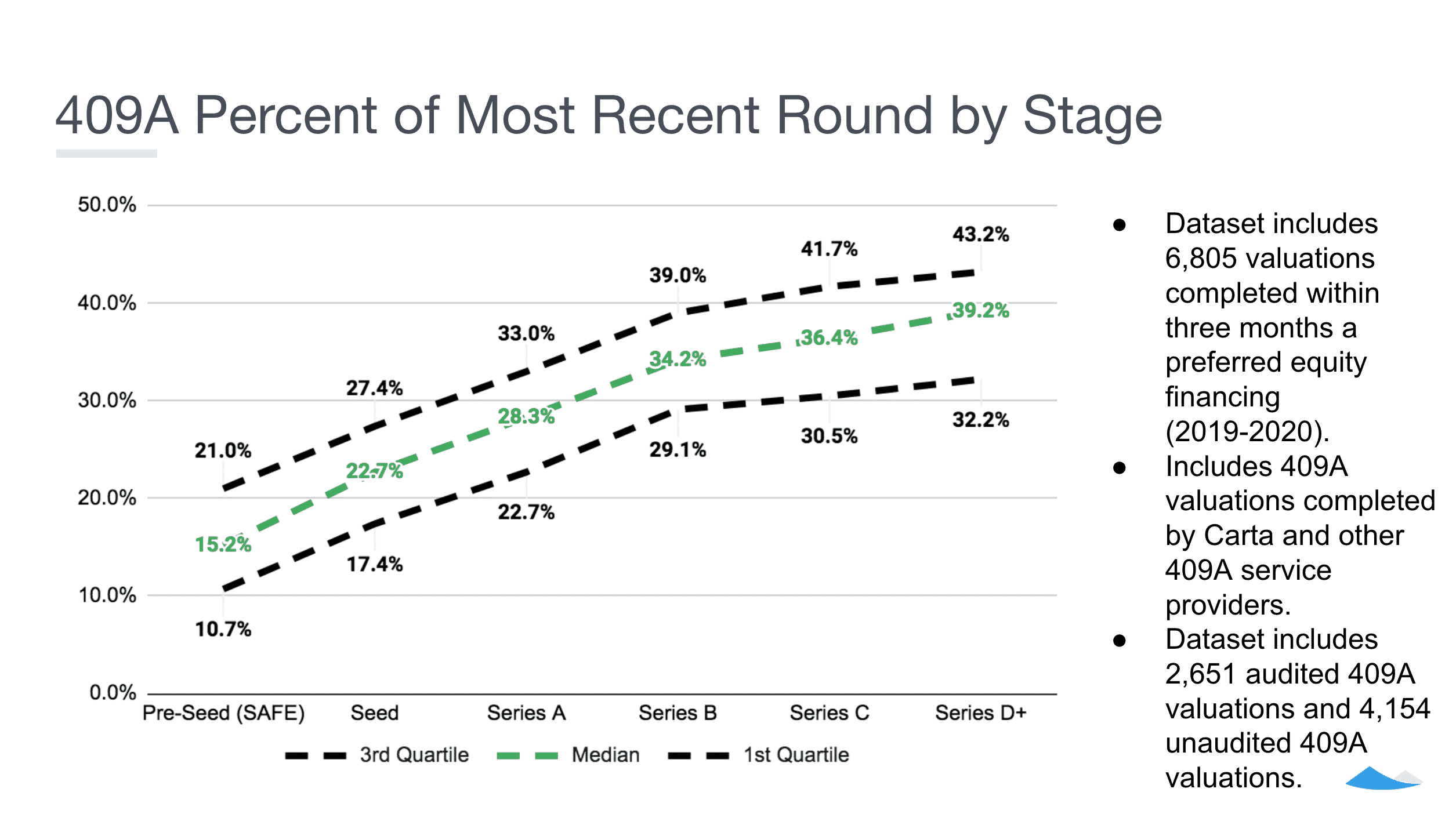

The discount of common stock versus preferred stock changes as a company evolves, with the deepest discounts in the early days. In fact, check out the graph below, produced by Carta. It shows discount information from 6,805 professional valuations. As you can see, during the pre-seed stage, the average discount is 85%.

But what if you don’t yet have preferred stock to use as a basis for applying the discount to derive a common stock price? One method I see startup attorneys, accountants and board directors use during the idea development, pre-seed, or very early seed stage is to assume a reasonable fundraising valuation and then apply a discount derivative method. Let’s look at an example for a company using the following assumptions:

But what if you don’t yet have preferred stock to use as a basis for applying the discount to derive a common stock price? One method I see startup attorneys, accountants and board directors use during the idea development, pre-seed, or very early seed stage is to assume a reasonable fundraising valuation and then apply a discount derivative method. Let’s look at an example for a company using the following assumptions:

- If they were to sell equity to investors, rather than use a convertible security, they could earn a $2M valuation

- Incorporated with 10M total shares of common stock and issued all stock into the company

Based on those assumptions, below is a step-by-step approach to deriving a price per common share:

- $2.0M / 10M shares = $0.20 per hypothetical Preferred share

- $0.20 discounted by 80% = $0.04 per Common share

The above method suggests this company would price their Common shares at 4 cents per share ($0.04). I actually think that if this company paid to have a professional valuation done to price their common shares, the answer could be considerably lower and you’ll see such an example below in the section titled “online valuation calculator”.

The method just described does not provide certain legal protections that could be important to you in the future. For more on that, see the section below titled “Professional Valuation”.

Setting the Stage

Initial Incorporation

If you incorporated as a Delaware C-corporation, you set a Par Value on your newly-created Common shares. The par value is almost never used in practical purposes but is intended to represent the nominal value of the shares and, therefore, the value the company agrees to never go below when selling the same class of shares.

Many startups set the Par Value at a fraction of a penny, like $0.0001 or even as low as $0.00001. If you multiply the par value times the total number of shares you incorporated with (usually a huge number like 10 million), the implied valuation of the company is still extremely low. Even as low as a hundreds of dollars. But realize that the par value isn’t intended to put a value on your company.

Par Value versus Fair Market Value

The par value and the current Fair Market Value (FMV) of your common shares are two different things. But in the early days before companies reach some amount of repeatable revenue per quarter, they often leave the two equal. How much can your business grow before you should start to escalate the FMV? It depends on who you ask and how conservative you want to be.

FMV becomes really important when issuing stock options to employees or advisors. That’s because the FMV price per share becomes the exercise price for those stock options. And even once you start to escalate the common stock FMV, the par value remains the same as it was originally set, with few exceptions.

Side Note: It is very important that you follow proper procedures when changing the FMV for your stock. So if you use one of the methods described in this article to make a change, make sure to work with your attorney to ensure the process is completed correctly. The paperwork is usually simple, but that doesn’t mean it’s not important.

Benefits of a Low FMV

Early stage startups can really benefit from having a low FMV because it means they’re able to issue stock options to new employees with an extremely low exercise price. And since these same employees probably aren’t getting cash compensation anywhere near the market rate (read my related article titled “Compensating Your First Employees When You Are Cash Poor“), granting equity with a low exercise price can be a key selling point. Just do the math on 100,000 shares granted to an employee with an exercise price of $0.001 per share. It will only cost that employee $100 to exercise the shares after they are vested!

After the startup has success and their FMV is boosted to just $1 per share, a future employee that gets the same 100,000 shares of stock options will be faced with a $100K exercise cost. Big difference.

More about Preferred Equity

This different class of shares that are sold to investors carries preferential rights, such as a liquidation preference (first money back), pro rata investment rights, special voting/blocking rights, anti-dilution rights, and more. That makes preferred stock much more desirable (valuable) than common stock. And as mentioned before, your fundraising valuation directly relates to the price that will be set for your preferred class of shares, not your common shares. If you are raising money using convertible securities (ie – Note or SAFE), you won’t create preferred shares for those investors until they convert to equity with a future round of funding. But this still means that the valuation cap you use for your convertible security shouldn’t be divided by your total number of common shares to come up with a per-share common price.

Share Pricing Methods

Following are the various methods I see used by startups and their attorneys, accountants and board directors to set a FMV for their common shares.

“Thumb in the Air” Method

This method can be helpful for a company that has made some progress since incorporation, but doesn’t yet have a reliable or repeatable method of generating revenue. “Progress” most likely means building a working prototype or beta version of your product, filing a provisional patent that has decent potential, or raising a pre-seed round of funding to have some runway to continue pursuit of your dream.

I’ve seen quite a few startups in this situation use what I call the “thumb in the air” method. For example, after accomplishing a couple of the things mentioned before, the company’s board of directors might decide to escalate the FMV from the original $0.0001 par value to $0.005. That’s a 50X increase in the FMV but, admittedly, there’s no scientific basis for the higher share price. Basically, the company and their board directors are trying to demonstrate that the company is more valuable and less risky than before, but without paying to have a professional valuation done.

Side Note: Even if you use this method to set a FMV, you still need to take the proper steps to ratify it. For C-corps that usually means some board approval. For LLCs it probably means following whatever is dictated in the Operating Agreement.

Online Valuation Calculator

A company named Capshare (since acquired by a Morgan Stanley company) used to offer a free, online 409A calculator. It was removed in mid-2020, but served as a valuable tool for early stage startups – either to help set their Common share price or serve as a sanity check for something like the thumb-in-the air method.

While the tool was still available, I ran a simulation for a hypothetical company that has 10 million units of equity on the cap table and assumes their likely fundraising valuation is $3M. The suggested fair market value for each common share of equity is $0.00289. You can see the full valuation report here. In case you’re curious about the inputs, I used the suggested defaults for all of the inputs that had them. For the weighted valuation section, I entered $0 for the downside scenario (Capshare’s suggestion), $3M for the midcase, and $4.5M for the upside. I left the default probabilities for each scenario the way Capshare suggested. So that at least gives you one example.

Using Convertible Note Valuation Caps

I sometimes find startups that say they priced their common shares at something like $0.30 per share because they’re raising a seed round of funding on convertible notes (or SAFEs) with a $3M valuation cap and they are incorporated with 10M issued shares ($3M / 10M shares = $0.30 per share). The math is correct but the logic is not, for two reasons. First, the valuation cap does not set the valuation of the company but rather serves as a future protection mechanism for the investor, in case the company’s Series A valuation is way higher than originally expected (see related article title “Justifying the Cap Amount in Your Convertible Note“). Second, and more importantly, the convertible notes don’t convert into common stock but rather preferred stock.

Having said this, if you are actively selling convertible notes of SAFEs to investors with a particular valuation cap, that cap amount could help you decide on a hypothetical valuation you might use if you did sell equity to investors instead. One approach would be to discount the valuation cap by something like 30% to reflect the range of future valuations the convertible securities might convert at. Remember, the valuation cap is the highest valuation that would be used in the future and all other possible scenarios are lower than that. Using the $3M valuation cap mentioned here and a 30% discount, you would follow the steps in the TL/DR section using $2.1M for the hypothetical valuation ($3.0M discounted 30%).

Professional Valuation

Even without an equity round of funding to trigger share repricing, it is strongly recommended to have a professional valuation at some point when you have a repeatable method of acquiring customers or your revenues reach something like $20K per month. It is called a “409A” valuation, after the corresponding section of the IRS code. I’m sure many on the conservative side would recommend doing it much sooner than $20K of monthly revenue. Possibly they are right. Once you get to $500K per year, you almost certainly want a professional valuation done every year. Those valuations will price all classes of shares and protect you against lawsuits or IRS/SEC claims that your stock is underpriced. If you’d like to learn more about that, do a search for the phrase “409A safe harbor”.

Side Note: Although I’ve been using revenue milestones as the potential trigger for changing the FMV of your common stock, it’s not the only potential trigger – just the most common (no pun intended). Other accomplishments that would be considered a considerable improvement in company value or considerable reduction in death risk could also be triggers.

You can have a local business valuation professional (check their credentials and certifications) do the work or can check out an online service like Carta as an alternative, if you’re willing to forgo the deeper and on-going relationship you can get with a local professional.

How can you determine the level of revenue that justifies valuing your stock the proper way? The answer requires a risk-reward evaluation. With many thousands of startups formed each year, the odds of an IRS audit are extremely low. In fact, I cannot find any cases in which the IRS took action against a startup for violation of their valuation rules. Also, the standard the IRS would apply in such a case is that your chosen valuation was either “grossly unreasonable” or that you didn’t make a “good faith effort” to value the shares. Although that’s a pretty high bar for the IRS to reach, it’s like various forms of insurance. They aren’t in place for what is likely to happen but rather what could happen.

Side Note: The bigger risk with not escalating the FMV of your Common shares as needed over time relates to fundraising and acquisition due diligence. A Series A or Series B institutional investor will want to see that you’ve been running the company by-the-book or close. Sophisticated acquirers will want the same. So my belief is that it’s not the IRS you should be worried about but rather sophisticated investors (ie – VC’s) and big company acquirers.

To be clear, a professional 409A is the only sure way to be fully compliant with the IRS, regardless of your company’s size.

Accidentally Jacking Up Your Common Share Price

I sometimes find a very early stage startup incorporated with 10M shares and with a common share price of $0.20 or higher. When I ask why the per-share price isn’t still a penny or less, they usually tell me they sold common class equity to an investor. Oops! It’s true that is an easy way to sell equity to an investor that immediately wants to be on a cap table versus investing on a convertible security (see related articles titled “Convertible Note Basics” and “Reviewing the SAFE Investment Instrument“). But it can have a negative consequence of jacking up your common share price due to the fact that you sold X percent equity for Y investment. That mathematically dictates the share price FMV.

A potential solution that I sometimes see used is to create a second class of common stock for the investors. The new Class B Common shares would have some special rights attached to them (ie – liquidation preference, pro rata investment right, board seat, etc) and that alone should allow you to price their stock using the mathematical formula while keeping a lower FMV for the regular, Class A Common shares held by your employees and advisors.

I’ve learned from corporate attorneys that a liquidation preference is the best special right to give the Class B shareholders, if the intent is to create a separation of FMV price. In other words, giving them information rights, a pro rata right and special voting rights might not fully accomplish the objective.

Side Note: This same situation happens with companies formed as LLC’s but only with Units as the individual element of equity. If you’re an LLC and you need to sell equity to an investor, consider creating Preferred Units for them with special rights versus the Common Units you and your co-founders hold (Class A versus Class B units would work the same way).

Here’s another risk. What if you later sell preferred shares in an equity round of funding (ie – Series A) and the resulting preferred share price is $0.25? A professional valuation will likely result in a common share FMV around $0.05. Oops! How are your employees with a stock option exercise price of $0.20 going to feel about their stock options now being “under water”! You and your board of directors are going to be faced with a repricing debate on former stock option grants. Believe me when I say that’s going to get the attention of your corporate attorney.

Summary

Let’s get back to the title of this article, which relates to pricing your stock in the early days. Although a professional valuation is the only fully-compliant method to value your shares after you’ve made any meaningful progress, most startups leave their common share FMV the same as par value until they have a working prototype of their product. At that point, they might use the the “thumb-in-the-air” method until reaching repeatable customer acquisition or raising an equity round of financing.

Whichever method is used, the newly-decided FMV becomes the exercise price that is used for stock option grants to new employees and advisors.

Any actions taken related to your stock/unit price must be done in conjunction with your accountant and attorney. And if your attorney isn’t a corporate attorney that understands the startup capitalization and early growth phase well, get one.

– – – – – – – – – – – –

Additional Insights from a Specialist

Special thanks to my friend and former business colleague, Shari Overstreet. At the time of this writing, Shari is Managing Director for The McLean Group’s valuation practice in Austin, Texas. Shari has certifications in accounting (CPA), business valuations (CVA) and M&A (CM&AA). Here’s what she has to add on the subject:

The question of when a company should start having a valuation performed by an expert is the salient point. Of course, the main driver of having a valuation requirement is compliance related, and, quite frankly, fairness, as options and equity interests are considered to be compensation. As Gordon mentions, challenges to valuations come from not only the IRS and SEC (and your accountants), but also appear in shareholder lawsuits for a variety of reasons.

In the old days (not so many years ago), most attorneys recommended having a business valuation expert perform the valuation when a company received their first institutional funding round. However, due to advances in the whole startup ecosystem, the financing requirements and vehicles for younger companies have changed, which means a company receiving its first institutional “A” round is, in many cases, equivalent to one receiving a “B” or “C” round several years ago, in terms of its business plan progression. This makes determining when to have a professional involved in determining the stock price all that much more difficult.

Additionally, as mentioned above, the financing vehicles have and are changing from “simple” preferred rounds to other types of financing, like convertible notes, etc., therefore, making the good old “rule of thumb” approaches not useful.

In all, my advice to a young company is to form a relationship early on with a business valuation firm. Doing so is just as important, if not more important, than having a relationship with an attorney or an accountant, esp. for startups. The reason it is so important is because as an entrepreneur, your potential (lifetime) wealth will come from the equity component of your company. It’s important to get it right. A good valuation expert will likely realize you’re a young company, and will price their work accordingly so they can grow with you. They will also serve as trusted advisers for other topics that can arise and they should work closely with your attorney and accountant.