Hopefully you are reading this before you decide how much to raise. I’m referring less to the earliest funding raised (perhaps from friends and family) just to get your minimum viable product (MVP) built, which in many cases costs little or nothing, and more thinking about raising money after your product is built and/or your initial validation is completed. But the basic concepts outlined in this article apply to later stages as well.

This article doesn’t describe the best fundraising vehicles and associated terms to use for seed-stage funding but two common ones are described in related articles: “Convertible Note Basics” and “Reviewing the SAFE Investment Instrument“.

Startups raise money for one of two reasons: they either WANT to or they NEED to. Raising money due to want usually means the startup has an opportunity to grow faster or accomplish more quicker, but actually doesn’t have to. This optionality is hugely valuable. Most startups raising money due to need. If they don’t, their bank account will dry up and they’ll have no choice but to pack up their toys and go home.

This article explores just one of the topics covered in Chapter 2 of my bestselling book “Startup Success – Funding the Early Stages”.

You can listen to this chapter now and if you’re interested in the book, you can find it on Amazon here.

If you’ve already decided to raise a round of funding, including a target amount to raise, you might be getting the obvious follow-up question: “Why is that the right amount?” It’s a very simple and justifiable question for the investor to ask, but it is commonly met with either puzzled looks or unacceptable responses from the founder. Don’t worry, I have some suggestions that will definitely help.

Disclaimer: The concepts described in this article are for a venture-fundable company. Many startups don’t have the makings of a high-growth, venture-funded business but can still evolve into a great company. Additionally, there are other forms of financing versus selling equity to venture-style investors.

How Much Should a Startup Raise for a Round of Funding?

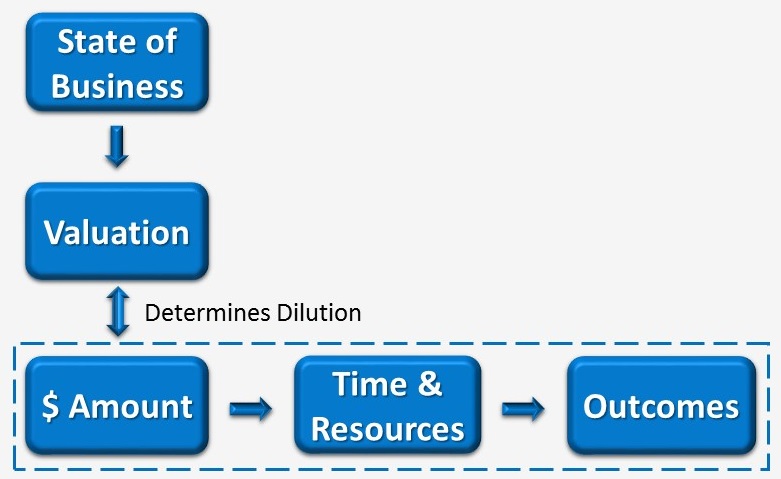

The graphic below summarizes the first major step in the exercise of deciding how much to raise. As you can see, it demonstrates the linear relationship between the amount raised, the time and resources gained and the expected outcomes you can accomplish with both time and resources.

Since you’re trying to solve for the right amount, let’s analyze the other two variables a little further.

Time & Resources

New funding will afford you a combination of more time (aka – runway) and more resources (headcount, marketing spend, etc). Interestingly, these two benefits are in opposition with each other. If you use all the new funding to dramatically increase your resources, you won’t gain hardly any additional runway. If, instead, you use all the funding for more runway, you won’t be able to add more resources. So part of the trick with optimizing this aspect of the exercise is to play a bunch of “what if?” scenarios with your financial forecasting model. But before you start doing that, keep reading, because there’s an approach to take that will give you an important starting point for this.

One problem I see is that many startups just pick an arbitrary amount of time and figure out how much money allows them to last that long. In fact, the amount of time is often a nice, logical 12 or 18 months. The problem is that’s too logical and I’ve already mentioned that investors care much less about how long your funding will last versus what you’re going to accomplish. So let’s look at the concept of “runway” differently.

If you force me to give typical runway projections based on funding stage, here is what I see most commonly:

- Pre-Seed: 6-9 months (often just enough time to get the product launched and gain the first paying customers)

- Early Seed: 9-12 months

- Late/Institutional Seed: 12-15 months

- Series A: 18-24 months

- Series B: 24+ months

Side Note: Although this article describes sequential rounds of funding, there is absolutely no rule that says you need to raise each mentioned round. For example, MANY startups bootstrap until needing to raise a Seed round of funding rather than raise a pre-seed round.

Outcomes

One of the most foundational things to remember is that investors care much less about how you are going to spend the money (activities) versus what you’re going to accomplish with their money (outcomes). What do I mean by “outcomes”? Well, how about acquiring a bunch of new customers, reaching a certain revenue milestone or becoming cash flow positive? How about securing a strategic partnership that provides significant leverage? How about getting FDA approval or approval on a patent filing? Those are all outcomes that reduce the investor’s risk and/or increase their upside investment potential.

So if an investor asks why you’re raising $____ (fill in your number), don’t rattle off a bunch of activities, but instead describe the expected  outcomes you’ll achieve in the future with the money raised.

outcomes you’ll achieve in the future with the money raised.

For a much deeper dive into this particular subject, read my related article titled “Investors Write Checks for Outcomes, not Activities“.

Work the Model Backwards

Rather than start this exercise from left ($ amount) to the right (outcomes), do the opposite. Start with a list of desirable outcomes, then determine the optimal combination of time and resources needed to accomplish those outcomes, then put a price tag on the whole exercise.

Easy, right? Well, you might already be wondering what sort of outcomes you should put on your starting list. To my way of thinking, the outcomes should be the things the next stage of investor wants to see in order to get excited about leading or participating in your next round of funding.

For example, if you had relationship-building meetings with potential future investors for your Series A round and a majority of them said they would get excited once you’re online marketplace reaches $1.5M in ARR, is launched in 5 geographical markets, and your new market activation playbook is both repeatable and optimized. Perfect. What combination of time and resources do you need to accomplish those things and how much funding with the resulting time/resources cost you?

Imagine only raising enough money to achieve $1.2M in ARR and being active in 3 geographical markets. Ouch! That’s going to put you in what I call the “fundraising chasm”. To learn more about the implications of falling in the fundraising chasm, read my article titled “Don’t Fall Into the Fundraising Chasm“.

Hopefully you realize the benefit of meeting with candidates for your next round of funding before raising your upcoming round. Not doing so leaves you guessing and mostly blind. Soliciting such meeting should start with something like “We’re not ready for you yet, but would love to tell you what we’re up to and get to know you for a time when we are ready.” Towards the end of the meeting, ask them what they would need to see to get excited about investing in a future funding round. If they give you an answer, ask them if there is anything else they would need to see.

A Needed Adjustment to Time/Runway

If you’re following the model, you’ve now back-solved for an ideal amount to raise. But there’s an adjustment you’ll need to make that relates to time/runway.

The fundraising activity itself takes time. It almost always takes at least 3 months and usually more like 5-6 months from start to finish. Because of this, you need to add at least that amount of time to your funding calculation. Otherwise, once you’re accomplished the desirable set of outcomes for the future investors, you won’t have any time to run that fundraising campaign. Starting the campaign 5-6 months early leaves you with unexciting accomplishments for them.

Again, run the exercise and then add a runway buffer to accommodate your future fundraising campaign. I recommend adding 6 months to be safe. This buffer will also help offset the negative impact of negative surprises or a needed pivot along the way, assuming it’s not a major pivot.

Another reason this runway buffer is important is because of negotiating leverage. If you wait until you’re 60 days from running out of cash (called the “cash fume” date) to start raising money, the investors will have all of the negotiating leverage.

Valuation & Dilution

Until this point, the exercise has been done in a utopian environment, without the impact of external influence. But once you take the strategy out on the road for investor meetings, two important words are going to enter the equation – VALUATION and DILUTION.

Dilution is a mathematical derivative involving valuation and new funding raised. The higher your valuation for a given amount of funding raised, the lower the dilution you and other existing shareholders will experience. And like many things that are negotiated, the valuation must seem fair to both sides (investor and company).

Valuation is driven, to a very large degree by both recent accomplishments and future expected outcomes. This is what I mean by “State of Business” in the graphic below. The state of your business includes recent financial and operational results (if your product is in the market and selling), the maturity of your management team and management system (tools, processes, etc), and also the future potential that is derived by those things.

I know, market size, business model, and many other factors also affect valuation. But those things are mostly unrelated to the amount of money you raise. Instead, it’s their potential positive influence on the future outcomes that help drive up your valuation.

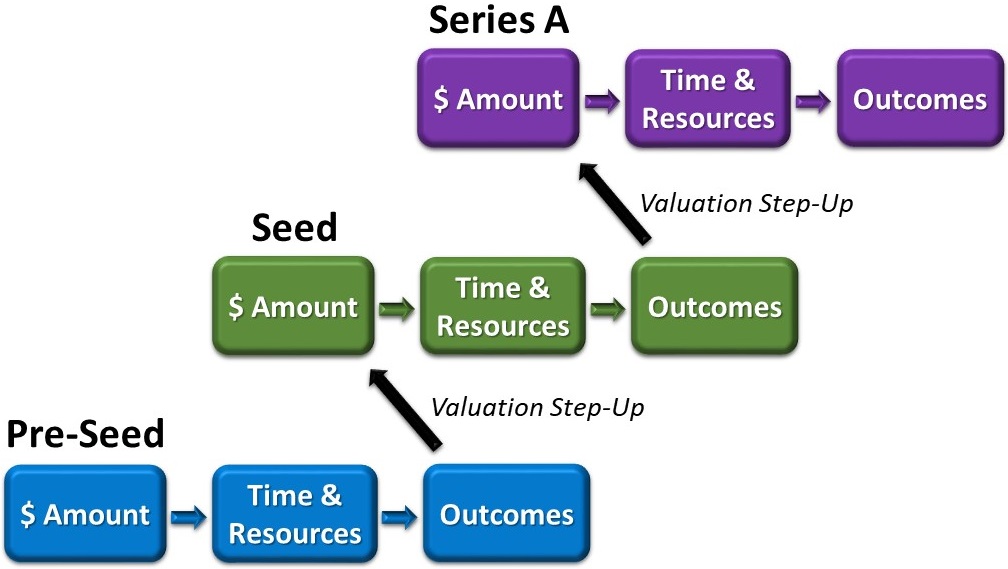

Multiple Funding Rounds Over Time

Now let’s project forward to see how multiple funding rounds tie together. With each round of funding, your projected outcomes eventually become the state of your business and that’s what you’ll use to gain a valuation step-up for the next round of funding. This cycle continues again and again until you no longer want, or need, to raise new funding.

A Final Word About Dilution

I find that a lot of fundraising founders get obsessively focused on dilution and make that the focal point for optimization. The problem with this approach is there are only two ways of optimizing for dilution. Either you push for a higher valuation, even if it’s not quite deserved (subjective issue) or you decide to raise less money than originally planned.

Pushing for an excessively high valuation will either cause your fundraising efforts to take longer, potentially eliminate investor prospects that could serve you best (provide the most value), and/or create a post-money valuation and future exit hurdle issue (described later in this article). If, instead, you decide to optimize dilution by raising less money, it will result in less runway and/or fewer and less significant outcomes – which will negatively affect your ability to raise funding in the future and maybe cause you to fall into the fundraising chasm.

As a result of what I’ve just described, I commonly preach the following mantra: Optimize for Growth, Not Dilution. A great company (culture, management system, etc) with a track record of strong growth has infinite options. That’s what you want and that’s what your investors also want.

Optimizing for growth includes partnering with the best investors that can help you grow a great company. In other words, I’ll take a combination of great investors whose valuation dilutes 25% versus so-so investors whose valuation only dilutes 22%.

When this exercise plays out as intended, each funding round yields a 2-3x step-up in valuation from the previous round, but only dilutes 20-30%. I’ll take that math all day long, while building a great company towards a great exit.

Note: Valuation is a very important term in a fundraising term sheet, but not the only one. It is critically important to understand how other terms in a term sheet can negate what seems like a good valuation. To understand that better, I highly recommend you also read my article titled “Tell Me Your Price and I’ll Tell You My Terms“.

A Trick for Calculating Dilution

Since dilution is dictated by the relationship between the new funding amount invested and the post-money valuation of the round (not pre-money), here’s a trick I use to quickly calculate dilution. Take the ratio of new funding to the pre-money valuation. Add 1 to the result and flip into a fraction. See examples below:

- 2x = 1/3 = 33% dilution

- 3x = 1/4 = 25% dilution

- 4x = 1/5 = 20% dilution

- 9x = 1/10 = 10% dilution

Hopefully you see the pattern. But to make double sure the method is clear, here’s an example:

- $5M funding at $15M pre-money valuation

- Ratio is 3X (15/5 = 3)

- Dilution fraction is 1/4

- Dilution to prior shareholders will be 25% (1/4 = 25%)

What About Excessive Dilution?

What if the valuations you’re getting from investors dilute 40-50%. Yikes, that’s painful! In this case, you probably need to iterate through the whole exercise again. This dilemma happens most often in the early seed stage. That’s because Series A investors have progressively positioned themselves later and later, in terms of needed traction and other accomplishments. I find that in the early seed stage it’s very difficult to secure enough funding at a reasonable valuation to reach the outcomes that get Series A investors excited.

For this reason, many startups break their seed stage into two sub-stages. The early seed stage is often funded by angel investors. Outcomes from that funding enables an institutional seed round from seed-stage VC’s. Outcomes from the institutional seed round get the company to the Series A sweet spot. Of course, there are differences in the specifics of this for hardware vs software vs deep tech and other types of startups. But the general concept still applies when the desired amount of funding isn’t met with an acceptable valuation.

If you’re facing this scenario, listen to my 5 minute podcast recording on this exact topic:

For more information about the Series A sweet spot, read my two articles titled “A Series A Sweet Spot Combines Size and Scope” and “Your Series A Readiness Scorecard“.

Core Principles Covered Thus Far

- Funding yields outcomes (via time and resources gained)

- Outcomes unlock future rounds of funding

- Raise enough to accomplish milestone outcomes that should also justify a meaningful future increase in valuation

- Optimize for growth, not dilution

Post-Money Valuation

If you’re raising money via a priced/equity round, the amount of money you raise directly affects your post-money valuation (pre-money valuation + amount raised = post-money valuation). Post-money valuation is often forgotten in the process, but it becomes extremely important when you’re ready to raise money again in the future. If you don’t create enough new value to exceed your post-money valuation by the time you need to raise again, you’ll have what’s called a “down round”.

If a down round happens after you’ve already sold Preferred equity to investors, it will have very negative implications. Your Preferred shareholders almost certainly have protectionist terms against a down round, which means the Common shareholders will take the biggest dilution hit that results. The amount of money you raise needs to give you enough new time and resources to comfortably exceed your current post-money valuation by the time you raise again in the future.

I’ll give a specific example to make sure this is clear. Let’s assume you raised $2M in institutional seed funding at a $6M pre-money valuation and expect it to give you 14 months of runway to accomplish significant milestones. Your post-money valuation will be $8M after that funding is completed. Approximately one year later when you are raising a $6M Series A (for example), you’ll want to be able to command a pre-money valuation considerably greater than $8M. In fact, you should be thinking in the $12M range at a minimum and will be hoping to justify $18M or more.

Prepare for Surprises

One final thought. The concepts mentioned here are actually as much art as science. You must allow for contingencies because things almost never play out like you expect. It’s impossible to predict how you will perform a year or more from now compared to your business plan projections. You can almost guarantee that things won’t work out exactly as planned, but in the early stages of growth it’s extremely hard to predict if the odds are higher of underperforming or over-performing.

Serial entrepreneur Jason Cohen wrote an interesting article that suggests that in either case you’ll either want or need more money. It’s titled “More money if you do, more money if you don’t“. Good food for thought and a nice demonstration of both the art and science of deciding how much to raise. The most common surprises and punches to the face I see are as follows:

- Product-market fit

After having some success with early adopter customers, you suddenly struggle to gain traction with your ideal target audience and determine changes are needed either to your product or target market. - Business model

The way you make money from your product gained initial traction but isn’t helping you scale like you predicted. Some change is needed. - Customer acquisition methods

You started selling one way (ie – inside sales only) but later determined that in order to win deals with larger companies using your highest priced offering, you need a field sales team or distribution channel (for example).

Forecasting the Future Cap Table

I previously mentioned my mantra “optimize for growth, not dilution“. However, I do recommend using a cap table calculator to run various scenarios and forecast what the cap table and various equity positions would look like after closing a particular funding round and maybe also the next one after that. You can find a link to one in the fundraising section of my Resources Page.

Summary

Fundraising is as much art as science (possibly more art in the earliest stages). Realize that many of the concepts described in this article are part of fundraising “science”. Every situation is very different. However, based on the core principles mentioned further above and the rest of the information described in this article, below is a step-by-step sequence to consider:

- Decide which meaningful outcomes can and should be achieved next (ones that get future investors excited)

- Determine the combination of time and resources needed to accomplish those outcomes

- Put a price tag on step #2 to determine the amount of money needed

- Include an extra buffer amount of money to allow for surprises and time to run your future fundraising campaign

- Sanity check the proposed amount based on a reasonable range of valuation and the resulting dilution – but while remembering to optimize for growth and building a great company

- Test drive these assumptions with real investors to determine if you have a decent chance of fundraising success

- If the result of #6 is positive, run the campaign. If not, determine if you can split your next stage of evolution into two stages, which means going back to step #1.