Are you scratching your head trying to figure out how convertible notes work? They are form of convertible security that is so commonly used for pre-seed and seed rounds of funding that every startup should understand them so that an appropriate set of terms can be incorporated.

This article includes an explanation of how convertible notes work and I’ve even included a quiz to test your knowledge and an FAQ to help you prepare for the most common questions investors ask, especially those that aren’t familiar with convertible notes.

For those interested in the seed-stage SAFE investment instrument made available by Y Combinator in December 2013 and later updated in 2018, ready my review and comparison to convertible notes here.

For those not already highly familiar with how convertible securities work, click the book cover image to read chapter 5 from my bestselling book on fundraising called Startup Success – Funding the Early Stages of Your Venture. The free chapter provides a full primer on convertible securities, including a comparison between the SAFE and convertible notes. Click here to order the book.

Or if you’re the audio book type, you can listen to the chapter here:

When To Use

A convertible note is a form of financing (fundraising) that is most commonly used in the earliest stages of company formation when the value (valuation) of the company is difficult or undesirable to establish. Setting a valuation for a company in the early stages is already more art than science but in the earliest stages it is almost all art. Actually, it’s purely the intersection of how much equity (ownership) the founders are willing to give up and how much equity the investor demands for their investment.

Another example of when convertible notes are sometimes used is for a “bridge round”, which is an attempt to bridge a short gap to the next desired equity round (for example, in between a Series A and a Series B). The extra time is usually desired to accomplish some important milestones that will give a bump up in valuation. Or maybe the company found itself with less runway than needed to reach the next equity round and needs extra cash to bridge the gap.

- For more on this read my article titled “Bridging a Gap Using a Convertible Note“

Another reason early stage startups like using convertible securities is due to an attribute known as the “rolling close”. Throughout the fundraising campaign, startups are able to “close” each individual investor and immediately put that new capital to use. This is very different than an equity round of funding, which has a minimum threshold that must be reached before a coordinated closing activity occurs and the new capital becomes available.

Some investors refuse to invest via convertible note because of the future uncertainty of how much equity they will eventually receive (explained in next section) while other investors have no issue with this fundraising instrument. It is somewhat of a religious debate and my FAQ at the end might help you prepare for this debate.

What Does It Convert To?

A convertible note is a form of debt (a loan). But instead of making regular payments to pay off the debt, the amount of the note “converts” to equity at a point in the future and as dictated by the various terms of the note. The class of equity shares granted per the conversion are the same as whatever the new equity investors are granted, which almost certainly means Preferred shares (versus Common shares). If the triggers for future conversion aren’t met, sometimes regular loan payments are required and sometimes conversion to equity happens anyway. But simply paying off the loan with interest isn’t the intent or hope for either the company or the investor.

How Much Should You Raise?

First, you need to do some deep thinking about how much money you should raise to support your next phase of growth (see related article titled “How Much Should You Raise?“). From there, you’ll also need to decide about a variety of terms and parameters of our convertible note. Let’s explore.

Standard Terms

The following terms are almost always included in a convertible note:

Conversion Triggers

Convertible notes almost always convert based on a length of time (aka “term” or “maturity date“) or the amount of money raised in a future equity round (called a “qualifying transaction” or “qualified financing“), whichever comes first. The length of time is usually in the 1-2 year range while a qualifying transaction is generally 2-3 times the amount to be raised on the note. In other words, if you’re raising $350K on a note you might set the qualifying transaction at $750K or $1M. If you raise that much in a future equity round, the note holders convert to equity.

Discount

It’s not fair that the early investors convert their invested amounts at the same valuation as the future investors. After all, the money from the early investors came at a time when the company’s viability was more risky and their investment facilitated company growth and other valuation-driving milestones. So the way to compensate for this is to give the convertible note investors a discount against the future valuation upon conversion.

Discounts are usually in the 15-20% range with 20% being most common. So if the company valuation for your future equity-based fundraising round is $5.0M and you offer a 20% discount, the convertible note investors will get equity based on a $4.0M valuation (20% off $5.0M).

Valuation Cap

What if the early-stage investments from convertible note investors allows the company to fly like a rocket ship and reach a valuation of something like $20M before raising their first equity-based round? It seems unfair that the convertible note investors convert at a $16M valuation (assuming 20% discount). So to offset this risk to the investors, most convertible notes include what’s called a valuation cap (aka – “cap”) to protect them.

Using an example of a $4M cap, if the company is able to raise a preferred equity round of funding from future investors at a valuation considerably higher than that, the convertible note investor’s investment converts assuming the valuation was only $4M. They would have been offered a discount anyway, so with a 20% discount the investor only gets to take advantage of the cap if the company raises their future equity round at a valuation higher than $5M (20% discount off $5M = $4M). In other words, the investor gets whichever is more favorable to them – the discounted valuation or the valuation cap.

- If you’re struggling to decide how to set the cap or are getting pushback from investors that it’s too high, see my related article titled “Justifying the Cap Amount in Your Convertible Note“.

- Realize that setting the cap way too low, even for just a subset of your seed investors, can cause big issues upon conversion to equity. When I say “way too low”, I mean a cap that could be 1/4 (or less) compared to the future pre-money valuation of your priced/equity round (for example, a $750K cap versus a future $3M pre-money valuation). The investors with the extremely low cap will get so much equity that the new lead investor for the priced/equity round might not be able to reach their required equity amount. They also could get end up with a 3X or 4X liquidation preference, which certainly isn’t intended but is usually a byproduct of the way convertible note terms are written (see Jose Ancer’s article describing “Liquidation Preference Overhang“)

Interest Rate

Like any form of debt, a convertible note carries an interest rate. The interest accrues until either the conversion takes place or the note is paid off. For a conversion, the interest is added to the initial investment before calculating how much equity to give. In other words, a $50K investment would convert at a value of something like $53-58K depending on the interest rate and how much time goes by before conversion. Typical interest rates for convertible notes are in the 6-8% range.

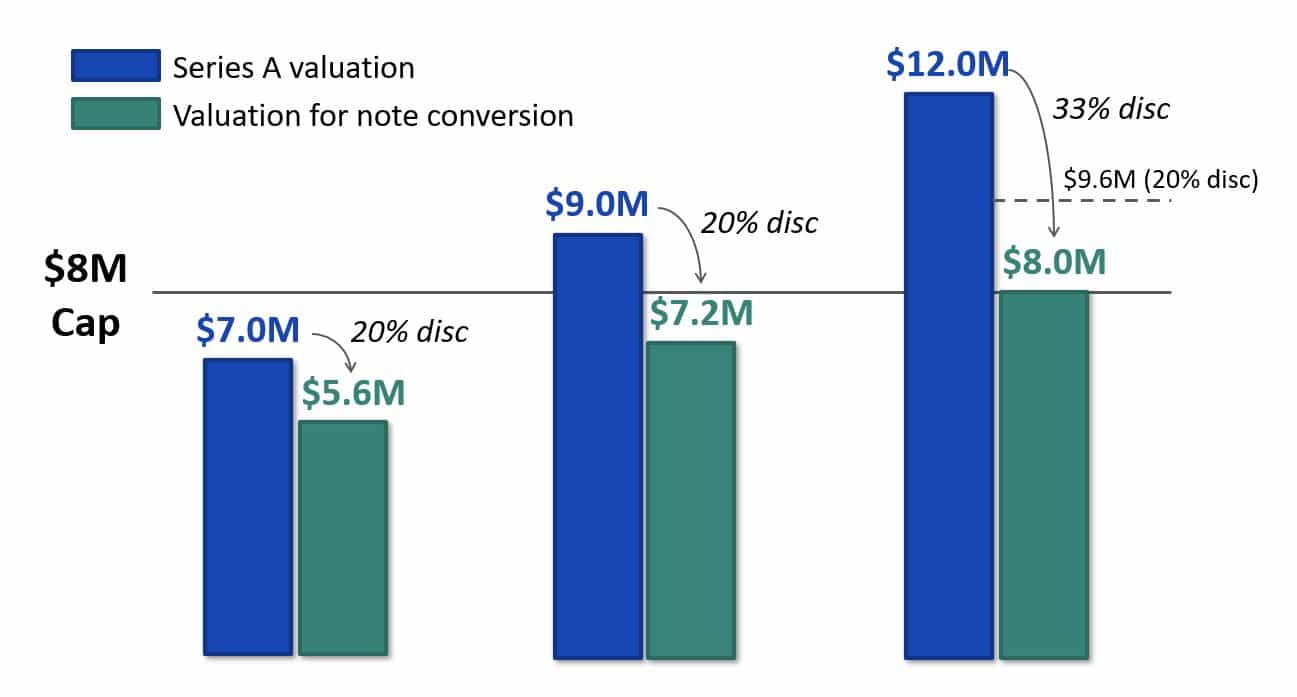

Visualizing the Discount – Cap Relationship

Refer to the graphic below to make sure you’re clear on the relationship between the discount and the valuation cap. In this scenario, the convertible note has a $8M valuation cap and a standard 20% discount. What you see are three different equity conversion scenarios, each with a different pre-money valuation for the equity round of funding that triggers conversion to equity. The valuation figures are just examples, and might be considerably higher or lower than your future Series A. Let’s review each scenario:

- $7.0M Valuation – Applying the 20% discount yields a $5.6M result. Since that is below the $8M valuation cap, the note holders convert to equity assuming a $5.6M valuation.

- $9.0M Valuation – Although the Series A valuation is higher than the cap, applying the 20% discount yields a $7.2M result. Since that is below the $8M valuation cap, the note holders convert to equity assuming a $7.2M valuation.

- $12.0M Valuation – Applying the 20% discount yields a $9.6M result. Since that is above the $8M valuation cap, the note holders convert to equity assuming an $8.0M valuation. Notice that this means the note holders get an effective discount of 33% instead of only 20%.

The lower the valuation figure that is used for calculating equity ownership (the post-money valuation), the higher the equity percentage will be. See below two examples:

- $1M investment divided by $10.0M post-money valuation = 10.0% ownership

- $1M investment divided by $8.0M post-money valuation = 12.5% ownership

Although the valuations included in convertible notes are typically expressed as pre-money figures, it is actually the post-money valuation for the equity funding round that determines equity ownership percentages. Additionally, from a technical perspective, the note holder’s discount gets applied to the resulting price-per-share that the new equity holders get (Series A investors in the above example) rather than the Series A pre-money valuation. The above graphic is a simplified example that is much simpler to explain the relationship between the discount and the valuation cap, but is not technically the way the mathematics are applied in real life.

If you would like to hear me describe the interactions between the Discount and the Valuation Cap using a different graphic, watch this short video I produced.

Optional Terms

Maximum Authorized Amount

Sometimes there is a stated limit to how much can be raised on the note. This might be referred to as the “aggregate principal amount” or might be described in a section labeled “closings” or “subsequent closings”. The objective of this term is to inform the investors how much you might raise in a particular round. There can be some psychology at play when setting this number. See my related article on this topic titled “Setting the Max Authorized Amount on Your Convertible Note“.

Early Exit Multiple

If included, this is described in a section usually labeled “Change of Control”. What if the company skyrockets and ends up being acquired for a decent amount of money before the term limit on the note and without ever needing to raise an equity round that would cause the conversion? It seems unfair that the early investors only get their initial investment back plus any accrued interest. So to reward the convertible note investors, it’s not uncommon to see an early exit multiple.

2X is fairly common for this (in other words, they double their money). An alternative is to give the investor an option to convert to equity using the stated cap as the valuation and let them participate in the acquisition with other equity holders, if this is more favorable than the early exit multiple.

End of Term Conversion

What happens if you reach the end of the term (maturity date) without a natural conversion? Your convertible note investors don’t typically want you to start making debt payments to them of principal plus interest and they don’t want you to ask them to agree to extending the maturity date (see related article titled “Extending Your Convertible Note“). They want equity (ownership) in your company and the hope for a big return in the future when you do an IPO at a $1B valuation.

Some convertible notes include the possibility of converting to Common class equity if the maturity date is reached without a natural conversion. What valuation assumption is used for this? Either the valuation cap amount or even a discount off the valuation cap (maybe the same discount as is stated in the convertible note). The reason for the discount is the likely scenario that the reason you weren’t able to raise money before the maturity date was reached is because you didn’t execute as well as expected. If so, why should the investor convert to equity using a high-side protection figure like the valuation cap? Instead, they should get some discount from that amount. At least that’s the argument from the investor’s side.

Most Favored Nations Right

What if you give investors a certain collection of terms and then later give a future investor better terms? An example would be a lower valuation cap for the future investor. That doesn’t seem fair to the earlier investors and the Most Favored Nations (MFN) right is intended to protect the earlier investors. It basically says you’ll adjust their terms to match the future investor, if they’re move favorable.

Legal Approvals and Filings

Whether you’re incorporated as an LLC or C-corp, you are probably required to document formal approval before raising funding on a convertible note. Check your bylaws (or operating agreement) and confirm with your attorney to make sure everything is done by-the-book. (for more on running a clean company, read my article titled “Accumulated By-the-Book Debt Eventually Comes Due“).

Most funding rounds using convertible notes are not filed with the SEC like equity funding rounds are. But there might be reasons why you should do so, including if you happen to need the Rule 506 Safe Harbor protection the comes with a Regulation D filing. Your attorney is, again, the best one to advise you on this.

Forecasting the Future Cap Table

I have a mantra that recommends entrepreneurs optimize for growth, not dilution. However, because of the various scenarios that might cause the valuation cap to come into play, I do recommend using a cap table calculator to run various scenarios and forecast what the post-Series A cap table and various equity positions would look like after the convertible notes convert to equity. You can find a link to one on my Resources Page.

Side Note: This might seem strange but there are actually three different approaches that can be used to determine the price per share (and therefore the ultimate % equity) for the note holders after conversion into equity. One method locks the pre-money valuation, one locks the post-money valuation and the final method is based on the dollars invested by the various constituents (note holders versus new equity investors). Read this article if you want to dive deeper into this somewhat-complicated topic.

Summary

Convertible notes are usually less complicated, and therefore less costly, to put together for the company. You don’t need to spend a lot of money on legal fees to put together a fundraising round using a convertible note. There are  online, open source templates if you’ll do a search. Make sure you understand everything in the template and at least get a legal review by an attorney before considering it final. And if you want to educate yourself on other aspects of venture financing, buy the book Venture Deals by Brad Feld and Jason Mendelson. You can find it here on Amazon.

online, open source templates if you’ll do a search. Make sure you understand everything in the template and at least get a legal review by an attorney before considering it final. And if you want to educate yourself on other aspects of venture financing, buy the book Venture Deals by Brad Feld and Jason Mendelson. You can find it here on Amazon.

If you are considering raising your funding round using another type of convertible security called a SAFE (simple agreement for future equity), you’ll want to learn about the differences between it and convertible notes in this article I wrote here.

——————————————

Think you’ve got it?

Test yourself with my online 8-question quiz.

——————————————

FAQ to Help with Investor Debates

Question: Why not just do a priced/equity round?

Answer: It will cost us considerably more in legal costs and requires us to set a valuation for the company at time when we don’t have much of a financial and operational track record to base it on. We would also need to create a new class of shares (Preferred shares) which come with various rights that we feel aren’t necessary or appropriate at this time.

blank line

Concern: I’m not interested in just getting a 7% interest rate return. Where’s my upside?

Response: The interest rate is not the most important term at all. The intent is for us to raise an equity round of financing in the future at a stated valuation. You will convert to equity at a discount versus the future investors and the interest that accrues simply increases your amount that converts to equity. When we build a great company and eventually exit for $1B, we will all make lots of money together.

blank line

Concern: A 20% discount doesn’t seem fair. You’re using my money to grow and potentially earn a high valuation in the future.

Response: If our valuation drives much above the valuation cap, causing the cap to come into play, your discount will be greater than 20%. For example, if we earn a valuation that is double the valuation cap, you would effectively be getting a 50% discount.

blank line

Concern: There’s some reasonable risk that things won’t work out and you might need to dissolve the company. In that event, I would rather be an equity holder to hopefully get some of my money back.

Response: Actually, you probably stand a better chance to get some money back following a dissolution if you sit as a holder of secured debt.

blank line

Concern: You might never raise an equity round of financing and I’ll be stuck holding a Note.

Response: (check the terms of your note to confirm some/all of this response is accurate) If the Note reaches the end of term (maturity date), you would have an option to convert to Common class equity using a formula that involves the valuation cap amount. You could also force us to pay you back principal + interest, although that is very uncommon. Instead, most Notes that reach maturity gain approval from investors to extend the maturity date. With the valuation cap in place, the investor is still has economic protection from any increases in valuation for a future equity round of funding that triggers conversion.

Side Note: If your Note does not have a valuation cap term, investors are likely to insist that one be added before they grant an extension to the maturity date.